If you’ve been on the fence about whether or not you will be doing a short sale then you NEED to read this!

If you’re not familiar the Mortgage Forgiveness Debt Relief Act (MFDRA) of 2007, it was passed by President Bush in December in an attempt to help homeowners who completed short sale transactions avoid a potentially hefty tax bill after the fact. It was one of the best pieces of legislation to help homeowners, in my opinion, and has helped many people significantly reduce any tax liability from a short sale.

How the MFDRA affects the homeowners today…

When a homeowner completes a short sale their lender will deal with their “loss” in one of a few ways. Either they will pursue the homeowner for the balance of the loan owed, or they will give the homeowner a 1099C for the amount they lost which is considered “forgiveness of debt”. The Mortgage Forgiveness Debt Relief Act deals with the 2nd scenerio where a 1009C is given to the homeowner.

The result of a 1099C in a short sale…

In many cases, prior to the MFDRA, when a homeowner received a 1099C after completing a short sale, the “forgiven amount” could be considered income (phantom income) by the IRS and taxes would be due for that amount. This created another hardship for many homeowners who escaped the clutches of foreclosure only the fall in the lap of the IRS with a large tax bill now due. Many homeowners decided to let their property go into foreclosure, and risk their bank coming after them for money rather than having the IRS chase them since, unlike the bank, ”their bite is worse then their bark”.

Hooray! Along comes the MFDRA!…

So when the government saw homeowners choosing to let lenders foreclose rather than risking their necks with the IRS they took action and this law came into existence. Homeowners who qualify for the protection under the MFDRA, when a short sale is completed and they receive a 1099C, that income would not be considered taxable. This took the burden off the backs of homeowners and incentivized working with lenders to complete short sales. This was done with hopes to help not only these homeowners, but also the housing market and our economy as a whole.

2012…the end of the…MFDRA!…

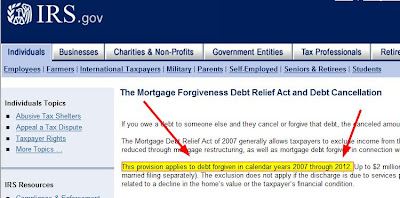

Unless there is another extension of the Mortgage Forgiveness Relief Act it’s provisions will end after 2012. That might seem like a long time from now, but consider the fact that a short sale transaction can take anywhere from 3-9 months sometimes more and sometimes less. This will depend on which lender is handling the process, how soon you receive and offer, and also who is handling the transaction.

With the amount of buyers that back out of short sales these days it’s advisable to NOT wait until you only have several months left to start the process. If a homeowner doesn’t make the deadline that could mean SERIOUS tax problems which could’ve been avoided. Many homeowners that want to keep their homes also apply for Loan Modifications in hopes that their situation will improve. At last check I remember hearing there is approx. a 42% success rate for homeowners who’ve completed a loan modification NOT falling back into a hardship. A loan modification can also take 3-6 months to get approved, usually will have a 90 day trial period (possibly longer), and if a homeowner doesn’t qualify they may find out that a short sale is their only option left!

Get it while the gettin’ is good!…

If you have been considering a short sale, but have been holding off, please take these points into consideration! If a short sale is not necessary in your situation then find a solution that is (i.e. loan modification, forebearance,etc.). Right now the economic climate is such that lenders and even Uncle Sam and the IRS are willing to help people with their financial situations, but as many of us know that can change over night! Understand the sense of urgency and take action! Contact a short sale specialist in your area to help guide you down this path and determine if it’s the right option for you and your family.

Don’t wait…2012 will be here before you know it and it may be too late!

PS- I seriously considered writing this “wake up call” to homeowners later on this year, but since I know how slow banks and some people are to respond I felt compelled to do it today! Take action! If you need advice or have questions contact me TODAY !

If you’re not familiar the Mortgage Forgiveness Debt Relief Act (MFDRA) of 2007, it was passed by President Bush in December in an attempt to help homeowners who completed short sale transactions avoid a potentially hefty tax bill after the fact. It was one of the best pieces of legislation to help homeowners, in my opinion, and has helped many people significantly reduce any tax liability from a short sale.

How the MFDRA affects the homeowners today…

When a homeowner completes a short sale their lender will deal with their “loss” in one of a few ways. Either they will pursue the homeowner for the balance of the loan owed, or they will give the homeowner a 1099C for the amount they lost which is considered “forgiveness of debt”. The Mortgage Forgiveness Debt Relief Act deals with the 2nd scenerio where a 1009C is given to the homeowner.

The result of a 1099C in a short sale…

In many cases, prior to the MFDRA, when a homeowner received a 1099C after completing a short sale, the “forgiven amount” could be considered income (phantom income) by the IRS and taxes would be due for that amount. This created another hardship for many homeowners who escaped the clutches of foreclosure only the fall in the lap of the IRS with a large tax bill now due. Many homeowners decided to let their property go into foreclosure, and risk their bank coming after them for money rather than having the IRS chase them since, unlike the bank, ”their bite is worse then their bark”.

Hooray! Along comes the MFDRA!…

So when the government saw homeowners choosing to let lenders foreclose rather than risking their necks with the IRS they took action and this law came into existence. Homeowners who qualify for the protection under the MFDRA, when a short sale is completed and they receive a 1099C, that income would not be considered taxable. This took the burden off the backs of homeowners and incentivized working with lenders to complete short sales. This was done with hopes to help not only these homeowners, but also the housing market and our economy as a whole.

2012…the end of the…MFDRA!…

Unless there is another extension of the Mortgage Forgiveness Relief Act it’s provisions will end after 2012. That might seem like a long time from now, but consider the fact that a short sale transaction can take anywhere from 3-9 months sometimes more and sometimes less. This will depend on which lender is handling the process, how soon you receive and offer, and also who is handling the transaction.

With the amount of buyers that back out of short sales these days it’s advisable to NOT wait until you only have several months left to start the process. If a homeowner doesn’t make the deadline that could mean SERIOUS tax problems which could’ve been avoided. Many homeowners that want to keep their homes also apply for Loan Modifications in hopes that their situation will improve. At last check I remember hearing there is approx. a 42% success rate for homeowners who’ve completed a loan modification NOT falling back into a hardship. A loan modification can also take 3-6 months to get approved, usually will have a 90 day trial period (possibly longer), and if a homeowner doesn’t qualify they may find out that a short sale is their only option left!

Get it while the gettin’ is good!…

If you have been considering a short sale, but have been holding off, please take these points into consideration! If a short sale is not necessary in your situation then find a solution that is (i.e. loan modification, forebearance,etc.). Right now the economic climate is such that lenders and even Uncle Sam and the IRS are willing to help people with their financial situations, but as many of us know that can change over night! Understand the sense of urgency and take action! Contact a short sale specialist in your area to help guide you down this path and determine if it’s the right option for you and your family.

Don’t wait…2012 will be here before you know it and it may be too late!

PS- I seriously considered writing this “wake up call” to homeowners later on this year, but since I know how slow banks and some people are to respond I felt compelled to do it today! Take action! If you need advice or have questions contact me TODAY !